Key Takeaways

- Credit management automation improves decision quality—not just operational efficiency. The greatest value comes from consistent, policy-driven credit decisions rather than simply accelerating approval workflows.

- Credit risk automation goes beyond workflow automation. While workflow automation digitizes tasks, credit risk automation continuously evaluates customer risk using centralized data, business rules, and ongoing monitoring.

- Successful automation platforms combine data, governance, and continuous risk monitoring. Finance leaders should evaluate solutions based on decision consistency, real-time risk visibility, ERP integration, and measurable financial outcomes.

- Technology alone won’t guarantee ROI. Organizations achieve better results when they simplify credit processes, improve data quality, and measure business outcomes such as bad debt reduction, policy compliance, and Days Sales Outstanding (DSO).

- The right vendor should strengthen your credit operating model, not just automate existing workflows. Asking the right evaluation questions helps finance teams identify solutions that improve governance, scalability, and long-term risk management.

Most organizations don’t struggle because they lack credit policies. They struggle because those policies become increasingly difficult to execute as the business grows.

A finance team may have clearly defined approval thresholds, customer risk categories, and credit review processes. Yet, as customer volumes increase, those standards are often applied inconsistently. Analysts work across spreadsheets, ERP systems, emails, CRM platforms, and external credit reports, making every decision dependent on how quickly information can be gathered and interpreted.

The result isn’t simply slower approvals. It creates inconsistent credit decisions, delayed customer onboarding, hidden portfolio risk, and growing administrative costs. More importantly, it forces experienced credit professionals to spend time collecting information rather than evaluating it.

This execution gap is why credit management automation has become a strategic investment rather than an operational upgrade. However, organizations evaluating automation often make one critical mistake—they focus on digitizing workflows instead of improving how credit decisions are made.

That distinction separates successful automation initiatives from projects that simply replace spreadsheets with software.

The Real Problem Isn’t Manual Work, It’s Inconsistent Decision Quality

Most discussions around credit risk automation emphasize efficiency: fewer manual tasks, faster approvals, and reduced paperwork.

While those outcomes are valuable, they rarely represent the strongest business case. The larger issue is decision quality.

Consider two credit analysts reviewing nearly identical customer applications. One approves the request based on historical payment performance, while the other requests additional financial documentation because recent exposure has increased. Neither decision is necessarily wrong, but inconsistent judgment creates unnecessary operational risk. As businesses scale, these inconsistencies multiply. Different business units interpret policies differently, customer information becomes fragmented across systems, and periodic credit reviews fail to capture rapidly changing financial conditions.

In other words, the challenge isn’t that credit policies don’t exist. It’s that they become difficult to enforce consistently.

Effective credit risk automation addresses this execution challenge by combining centralized customer data, standardized decision rules, and continuous monitoring into a single operating model. Routine decisions follow predefined governance, while experienced analysts focus their expertise on complex or high-value accounts. The outcome isn’t simply faster approvals—it is greater consistency across every credit decision.

Workflow Automation and Credit Risk Automation Are Not the Same Thing

One of the biggest misconceptions in the market is treating workflow automation and credit risk automation as interchangeable. Workflow automation digitizes tasks. It routes approvals, assigns work, sends notifications, and replaces manual emails with structured processes.

Credit risk automation goes much further. It improves the quality of decisions themselves. Before investing in any platform, finance leaders should understand this difference.

| Workflow Automation | Credit Risk Automation |

| Digitizes approval workflows | Continuously evaluates customer risk |

| Automates document routing | Applies policy-driven decision rules |

| Reduces administrative effort | Improves consistency across credit decisions |

| Focuses on operational efficiency | Focuses on portfolio risk and financial outcomes |

| Measures processing speed | Measures decision quality, exposure, and policy compliance |

Many organizations successfully automate approvals but continue making decisions based on outdated financial information. While the process becomes faster, the underlying credit strategy remains unchanged.

Organizations generating the highest return from automation invest in platforms that continuously reassess customer risk rather than simply accelerating existing workflows.

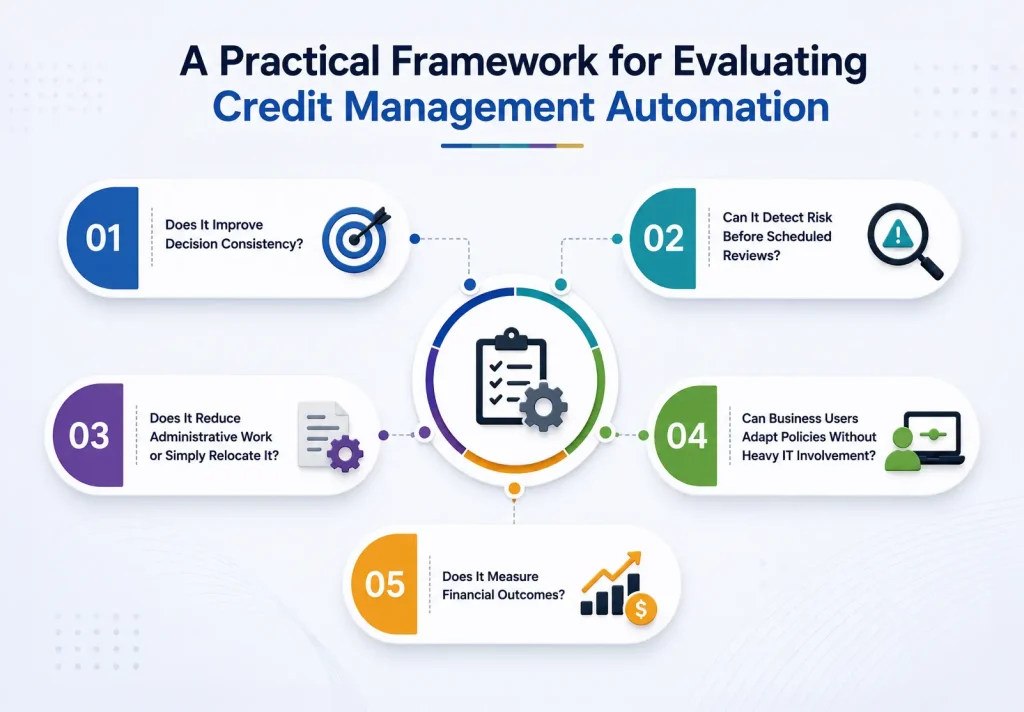

A Practical Framework for Evaluating Credit Management Automation

Feature lists rarely help finance leaders select the right platform. Instead of asking whether a solution includes AI, dashboards, or workflow automation, evaluate whether it strengthens five core capabilities.

1. Does It Improve Decision Consistency?

The objective isn’t to replace analyst judgment but to ensure similar customers receive similar evaluations. Strong platforms embed credit policies into configurable business rules while allowing analysts to review strategic exceptions.

2. Can It Detect Risk Before Scheduled Reviews?

Annual or quarterly credit reviews no longer reflect today’s business environment. Customer financial health can change rapidly due to market conditions, supply chain disruptions, or shifting payment behavior.

Solutions that continuously monitor payment performance, outstanding exposure, and external credit signals enable organizations to respond before financial issues affect cash flow.

3. Does It Reduce Administrative Work or Simply Relocate It?

Some platforms automate approvals but still require analysts to gather financial documents manually or update customer information across multiple systems.

True credit risk automation minimizes repetitive activities by consolidating relevant data into a unified customer profile, allowing analysts to focus on risk evaluation rather than administration.

4. Can Business Users Adapt Policies Without Heavy IT Involvement?

Credit policies evolve alongside business strategy. Organizations should evaluate how easily finance teams can modify approval rules, exposure thresholds, escalation paths, and review frequencies without relying on lengthy development cycles.

5. Does It Measure Financial Outcomes?

The most valuable automation initiatives improve more than productivity. Finance leaders should evaluate whether the platform supports measurable improvements in bad debt reduction, policy compliance, portfolio visibility, and Days Sales Outstanding (DSO)—not just approval speed.

Three Mistakes That Reduce Automation ROI

Even well-planned automation projects can underperform when organizations focus on technology before operating model design.

1. Automating Inefficient Processes

Automation accelerates execution—it does not correct poor workflows. If approvals contain unnecessary reviews or inconsistent policies, software simply enables those inefficiencies to occur faster.

2. Measuring the Wrong Success Metrics

Organizations frequently celebrate faster credit approvals while overlooking more meaningful outcomes. A mature automation strategy should also reduce policy exceptions, improve portfolio visibility, identify deteriorating accounts earlier, and strengthen governance across the credit lifecycle.

3. Assuming AI Automatically Improves Credit Decisions

Artificial intelligence is a powerful capability, but only when supported by reliable data and well-defined policies. Organizations with inconsistent customer records or unclear approval criteria are unlikely to realize value from advanced analytics until they address those foundational issues.

Successful automation begins with process maturity and high-quality data before introducing increasingly sophisticated decision intelligence.

Questions Every Finance Leader Should Ask Before Selecting a Vendor

Technology demonstrations often highlight dashboards, automation workflows, and AI capabilities. However, the more valuable questions focus on long-term operational outcomes.

Before selecting a solution, ask vendors:

- How does the platform improve decision consistency across business units?

- Which customer risk indicators are monitored continuously rather than periodically?

- Can finance teams update credit policies without relying on IT resources?

- How are policy exceptions documented for audit and compliance purposes?

- Which KPIs have customers improved beyond approval speed?

- How does the platform support analysts instead of replacing them?

- What percentage of routine credit decisions can realistically be automated while maintaining governance?

These questions shift the conversation from software functionality to measurable business value—an important distinction during vendor evaluation.

Conclusion

The future of credit management is not defined by faster approvals alone. It is defined by better decisions.

Organizations that continue relying on fragmented data, periodic reviews, and manual policy enforcement will find it increasingly difficult to manage customer risk as their business grows. In contrast, businesses adopting credit management automation are moving toward continuous, policy-driven decision-making that strengthens governance while improving operational efficiency.

The highest value of credit risk automation is not that it replaces analysts—it enables them to spend less time managing processes and more time managing risk. For finance leaders evaluating automation, the most important decision is not which platform offers the longest feature list, but which solution consistently improves decision quality, adapts to changing business conditions, and supports sustainable growth.