Key Takeaways

- Finance data quality is fundamentally a trust issue, not just a data cleanup challenge. Sustainable improvements come from preventing data divergence rather than repeatedly correcting errors after they occur.

- Automation strengthens finance data quality by validating information at the point of entry, automating reconciliations, standardizing records, and continuously monitoring data integrity across systems.

- High-quality finance data should consistently meet five essential criteria—accuracy, completeness, consistency, timeliness, and auditability—to support confident financial reporting and decision-making.

- The greatest value of automation isn’t simply reducing manual effort; it’s enabling finance teams to spend less time reconciling data and more time analyzing business performance and driving strategic outcomes.

- When evaluating automation solutions, finance leaders should prioritize capabilities such as configurable validation rules, seamless integrations, scalable matching logic, transparent audit trails, and robust exception management over feature lists alone.

Every finance team says it has a finance data quality problem. Almost none of them have actually named it.

They call it “cleanup”. They call it “reconciliation”. They call it “just how close a week goes”. What they rarely call it—even though it’s the more accurate term—is a trust deficit.

Poor finance data quality doesn’t fail loudly. It fails quietly, in the form of a CFO who double-checks a number before presenting it, a board deck filled with footnotes and caveats, or an audit that stretches weeks longer than expected. The cost rarely appears as a visible line item. Instead, it shows up as hesitation, delayed decisions, compliance risks, and countless hours spent validating information that should already be reliable.

Improving finance data quality isn’t simply about correcting inaccurate records or eliminating duplicate entries. It’s about creating a financial ecosystem where every report, forecast, and transaction is built on trusted, consistent, and validated data. Without that foundation, even the most advanced analytics, ERP systems, and automation initiatives struggle to deliver meaningful business value.

If you’re evaluating automation to improve finance data quality, you’re really evaluating something much bigger: how much confidence your organization can place in its financial information without requiring a human to verify it first. That’s the perspective this guide takes. Rather than asking, “How do we clean data faster?”, it explores a more strategic question: “How do we build finance data that no one feels the need to double-check?”

The Real Failure Point: Finance Data Doesn’t Break; It Diverges

Most write-ups on this topic list the usual suspects — fragmented systems, manual entry, siloed ownership — as if they’re independent problems. They’re not. They’re symptoms of one structural issue: your systems of record don’t agree with each other, and nothing is watching for the moment they stop agreeing.

Call it data divergence. It shows up in predictable places:

- Fragmented source systems that were never designed to reconcile with each other — CRM, procurement, banking, and the general ledger each keeping their own version of “the truth”.

- Manual reconciliation, which doesn’t just cost time — it re-introduces error every time a human re-keys or re-matches a record, meaning the “fix” is itself a new failure point.

- Inconsistent entry standards, where “Acme Corp”, “ACME Corp”, and “Acme Corporation” are three vendors to your system and one vendor to reality.

- Delayed detection, where the first person to notice a data quality issue is an auditor, not your team.

- Diffuse ownership, where a problem that touches five systems belongs, in practice, to no one.

None of these is a data problem in isolation. They’re all the same problem – divergence without detection, just in different forms. That reframe matters, because it changes what you’re actually shopping for. You’re not looking for a cleanup tool. You’re looking for a detection layer.

The Five-Layer Test for “Good” Finance Data

Rather than treating data quality as a vague aspiration, it helps to test it against five concrete criteria — consider these to be the minimum bar, not the ambition:

- Accuracy — the data correctly reflects the underlying transaction or event.

- Completeness — no missing fields, records, or gaps in the reporting period.

- Consistency — the same entity, category, or metric looks identical everywhere it appears.

- Timeliness — the data is ready when the decision is made, not after.

- Auditability — every number has a visible line back to its source and the logic applied to it.

Here’s the uncomfortable part: manual processes can usually hit two or three of these on a good week. They almost never sustain all five every cycle at scale — because the fifth one, auditability, requires a level of documentation discipline that humans reliably deprioritise under deadline pressure. This is the gap automation is built to close, and it’s the only realistic way to do so at scale.

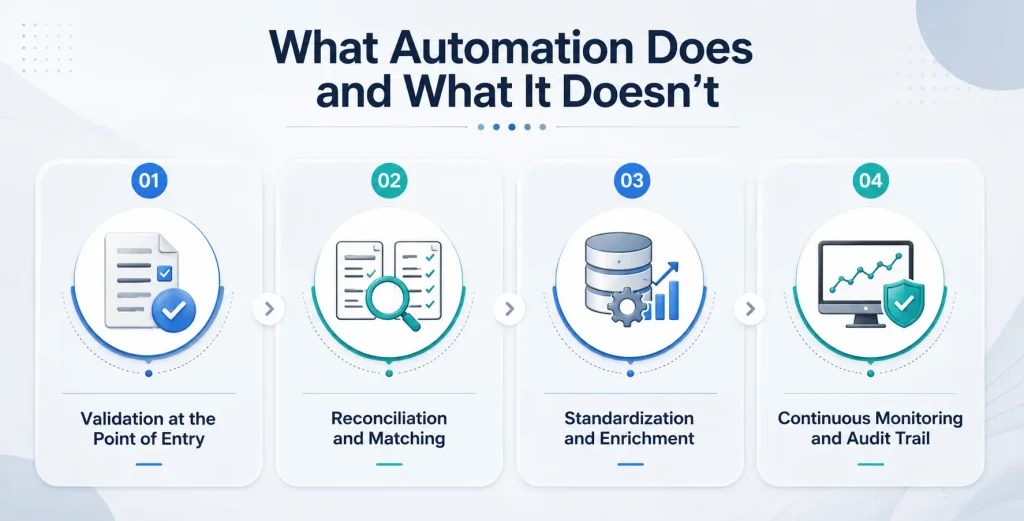

What Automation Does and What It Doesn’t

Automation is not a single button that produces ‘clean data.’ It’s a layer that intervenes at four specific points in the data lifecycle, and understanding the difference matters when you’re evaluating vendors who like to blur them together.

1. Validation at the Point of Entry

Errors get caught the moment data enters the system—duplicate records, out-of-range values, and malformed fields—instead of surfacing three weeks later in a close review. This is the single highest-leverage shift in the whole framework: it moves error detection from reactive to preventive, which is the difference between finding a fire and preventing one.

2. Reconciliation and Matching

Automated matching engines compare records across systems — bank feed to ledger, invoice to purchase order, subledger to general ledger — using configurable rules and, increasingly, models that improve match rates as they process more data. The work that used to consume a team for days becomes a review-by-exception task measured in hours.

3. Standardization and Enrichment

Vendor names, currency formats, cost center codes — all normalized against a single master reference, so “three spellings of the same vendor” stops being a permanent tax on every report that touches procurement data.

4. Continuous Monitoring and Audit Trail

This process involves ongoing monitoring, not just a one-time check — flagging drift or anomalies as they emerge and logging every transformation applied to the data, ensuring nothing is a black box when an auditor asks, “How did we get this number?”

What automation doesn’t do is remove the need for financial judgment. It removes the need for financial judgment to be spent on policing spreadsheets — and redirects it to the analysis that actually requires a human.

Manual vs. Automated: What Actually Changes

| Dimension | Manual Process | Automated Process |

| Error detection | Discovered during review or audit | Flagged at point of entry |

| Reconciliation speed | Days, often repeated each cycle | Hours, with exception-based review |

| Consistency across systems | Dependent on individual diligence | Enforced through standardization rules |

| Audit trail | Manually documented, often incomplete | Automatically logged and traceable |

| Scalability | Degrades as data volume grows | Scales with configurable rules and thresholds |

| Team focus | Finding and fixing errors | Analyzing clean data |

The number that should actually change your mind isn’t in this table — it’s the one you’d get by tracking how many hours your team spends each month reconciling versus analyzing. Most finance leaders have never measured that ratio. It’s worth measuring before you buy anything.

What This Looks Like When It Works

Consider a mid-sized organization closing its books across four business units, each running its own ERP instance. Before automation, a close week meant manually exporting data from each system, reconciling intercompany transactions in spreadsheets, and discovering mismatches late enough in the cycle to push the close out by several days — a pattern the team had quietly accepted as normal.

After introducing automated validation and reconciliation:

- Intercompany mismatches were flagged and routed for review as they occurred, not discovered during final reconciliation.

- Standardized vendor and cost-center reference data eliminated a recurring category of manual cleanup entirely.

- The team’s close-week effort shifted from data chasing to variance analysis — the work finance actually exists to do.

The headline result wasn’t a faster close. It was close; the team could defend without hedging — because every number carried a visible, traceable path back to its source. Speed was the side effect. Confidence was the point.

The Six Questions That Actually Separate Vendors

Most evaluation checklists ask about features. The better question is whether a vendor’s answers hold up under a follow-up question. Ask these, and push on the answers

- Rule configurability. Can your team define and adjust validation and matching rules without opening an engineering ticket every time?

- Integration depth. Does it connect natively to your ERP, banking feeds, and data warehouse — or does “integration” mean a middleware layer you’ll be maintaining in a year?

- Exception handling workflow. When something gets flagged, who sees it? Who resolves it? And is that resolution itself logged and auditable, or does it disappear into someone’s inbox?

- Scalability of matching logic. Does match accuracy hold as transaction volume and source-system complexity grow, or does it quietly degrade past a certain scale?

- Transparency and auditability. Can every automated decision be explained to an auditor in plain language, or does it require the vendor’s engineering team to interpret it?

- Change management support. Is there a real plan for migrating existing rules, historical data, and team workflows — or is “implementation” a euphemism for “your team figures it out”?

A vendor with a strong product will welcome these questions. A vendor with a strong demo will redirect you back to the feature list.

Where This Leaves You

Finance data quality isn’t a project you finish. It’s a discipline you either build into the system or keep re-performing manually, cycle after cycle, at a cost that never shows up as its own line item. Automation doesn’t remove the discipline — it changes what maintaining it requires: fewer hours spent chasing divergence, standards enforced by design instead of by diligence, and an audit trail that holds up without anyone having to reconstruct it after the fact.

The organizations that get this right don’t call their finance data “clean”. They describe it as something closer to boring nobody double-checks it, because nobody has a reason to.

If you’re at the point of comparing how to close that gap, the useful next step isn’t another feature checklist. It’s mapping your specific reconciliation and validation failure points against the five-layer test above and being honest about which layers you’re currently missing.

Would you like a second opinion on that mapping? Our team regularly collaborates with finance leaders to pressure-test current-state data quality gaps against what automation can realistically address. Reach out, and we will walk through your current close process and outline a credible path forward.