Key Takeaways

- Month end close automation delivers more than faster financial closes by improving accuracy, strengthening governance, and making hidden process risks visible before they become larger issues.

- Successful automation should focus on exception management, proactive variance analysis, and continuous validation of recurring journal entries rather than simply reducing manual effort.

- When evaluating automation platforms, prioritize capabilities that improve audit readiness, enforce accountability, and surface reconciliation exceptions instead of only measuring speed improvements.

- A meaningful ROI extends beyond labor savings to include reduced rework, improved compliance, stronger audit trails, and the ability to identify financial risks before they affect reporting.

- Organizations that combine automation with standardized close processes and ongoing governance build a more resilient finance function capable of delivering timely, accurate, and trustworthy financial reporting.

Month end close automation is transforming one of the most critical yet time-intensive processes in finance. As organizations manage growing transaction volumes, complex regulatory requirements, and increasing demands for faster financial insights, traditional manual close processes often create delays, errors, and unnecessary pressure on finance teams. By automating repetitive tasks such as reconciliations, journal entries, data validation, and report generation, businesses can accelerate the financial close while improving accuracy, compliance, and visibility across the organization.

This guide explores how month end close automation helps finance teams streamline workflows, reduce manual effort, strengthen financial controls, and deliver timely, reliable financial reporting. Whether you’re looking to shorten your close cycle or build a more agile finance function, adopting the right automation strategy can unlock significant operational and strategic value.

The Three Places Where Close Debt Hides

Month-end close is one of the most standardized processes in finance, yet it’s also one of the easiest places for hidden operational debt to accumulate. Every month, finance teams complete reconciliations, post journal entries, investigate variances, and prepare reports. When these activities rely on manual workarounds, undocumented assumptions, or outdated templates, they create what can be thought of as ‘close debt’—small process issues that compound over time without attracting attention.

Unlike obvious accounting errors, close debt rarely appears as a failed audit or a materially misstated financial statement on day one. Instead, it gradually erodes confidence in the close process, increases reliance on tribal knowledge, and makes every reporting cycle more difficult than the last. This is where month end close automation delivers its greatest value. While faster close cycles are important, the real benefit lies in creating consistent, repeatable processes that expose hidden risks before they become larger financial or compliance issues.

1. The reconciliation that “always matches”

Every finance team has accounts that someone reconciles almost from memory because they have always balanced. The process becomes routine enough that supporting documentation receives less scrutiny, and exceptions are often assumed to be timing differences without proper investigation.

This approach works—until it doesn’t.

A minor change in transaction flow, a new business entity, or an integration issue can introduce discrepancies that remain unnoticed for several reporting periods. By the time someone discovers the issue, multiple months may require correction, making root-cause analysis significantly more difficult.

Effective month end close automation removes this dependency on assumptions. Automated reconciliation engines compare transactions against predefined rules every cycle, flag unmatched items immediately, and require documented resolution before accounts can be marked complete. Rather than trusting historical patterns, automation validates every reconciliation using current data.

The objective isn’t to replace accountants’ judgment—it’s to ensure that judgment is applied where it’s needed most instead of repeating routine validation tasks.

2. Variance explanations written after the numbers

Variance analysis should help finance teams understand why financial performance changed. Too often, however, commentary is created only after numbers have already been reported to management.

At that stage, explanations become narratives rather than analysis. Instead of influencing financial reporting, they’re simply documenting what has already been accepted.

Modern close automation changes this sequence. Significant fluctuations are identified as transactions are processed, allowing finance teams to investigate unusual movements before reports are finalized. Threshold-based alerts can notify reviewers whenever balances exceed predefined tolerances, ensuring unusual activity receives attention before the close is completed.

This proactive approach improves both reporting quality and decision-making. Instead of explanations prepared after the fact, leadership receives numbers that have already been questioned, validated, and supported by evidence.

More importantly, finance professionals spend less time defending historical results and more time understanding what is actually driving business performance.

3. The journal entry template nobody reviewed

Recurring journal entries are among the biggest productivity gains in finance automation. Standardised templates can automatically generate accruals, allocations, depreciation, prepaid expenses, and intercompany adjustments.

The risk is that templates rarely receive the same attention after implementation.

Businesses evolve continuously. They acquire companies, launch new products, restructure departments, modify their chart of accounts, or enter new markets. A journal entry template created two years ago may continue processing successfully every month while gradually becoming less accurate.

Because the process is automated, the incorrect logic often appears trustworthy simply because it executes consistently.

Strong month end close automation includes governance around recurring entries. It tracks when templates were last reviewed, identifies changes to related accounts or organizational structures, and prompts finance teams to validate recurring journals whenever business conditions change.

Automation should not simply repeat existing processes faster—it should ensure those processes remain relevant as the organization evolves.

Together, these three examples demonstrate an important principle. Most close delays do not stem from a lack of effort by finance teams. They’re caused by manual processes that make hidden risks difficult to identify until they become costly problems.

The best automation platforms don’t just accelerate the close—they make uncertainty visible.

What This Means for How You Evaluate a Platform

Once you use close debt as the lens, the evaluation questions change. Instead of asking, “does it reconcile faster?” ask “does it make it harder to fake a reconciliation?” Use this table as a working diagnostic, not a checkbox exercise — score each vendor on whether the capability actually reduces close debt, not just close time.

| Capability | The Speed Question Everyone Asks | The Close-Debt Question Worth Asking |

| Reconciliation | Can it auto-match transactions? | Does it force a documented exception path or let stale matches roll forward silently? |

| Journal entries | Can it template recurring entries? | Does it flag templates that haven’t been reviewed in N months against a changed chart of accounts? |

| Variance analysis | Can it flag threshold breaches? | Does it flag before the number is reported, with a required explanation field, or after? |

| Workflow | Can it assign and track tasks? | Does it show who approved what without review, not just who approved on time? |

| Audit trail | Does it log activity? | Is the log immutable, or can entries be edited after the fact without a visible trace? |

| Integration | Does it connect to your ERP? | Does it flag data it couldn’t reconcile automatically, or does it silently drop exceptions? |

The right-hand column is where platforms actually separate from each other. Almost every vendor can answer yes to the left column. Far fewer can answer yes to the right one, and the ones that can’t will usually reframe the question rather than answer it directly. That reframe is itself useful information.

Calculating ROI Without Fooling Yourself

Time saved is the easy part of the business case. Build it, but don’t stop there:

- Hours saved per cycle = (reduced close days) × (people involved) × (loaded cost).

- Rework cost avoided — time spent finding and fixing errors that a manual process would have caught late or not at all.

- Audit friction reduced—hours spent reconstructing documentation versus having it exist automatically and immutably as work happens.

- Debt discovered, not just debt avoided — the honest version of ROI includes the value of finding a problem before an auditor or a restatement does. This number is harder to quantify and more important than the other three.

A vendor that only wants to talk about the first bullet is selling you speed. A vendor willing to talk about the fourth is selling you something closer to what you actually need.

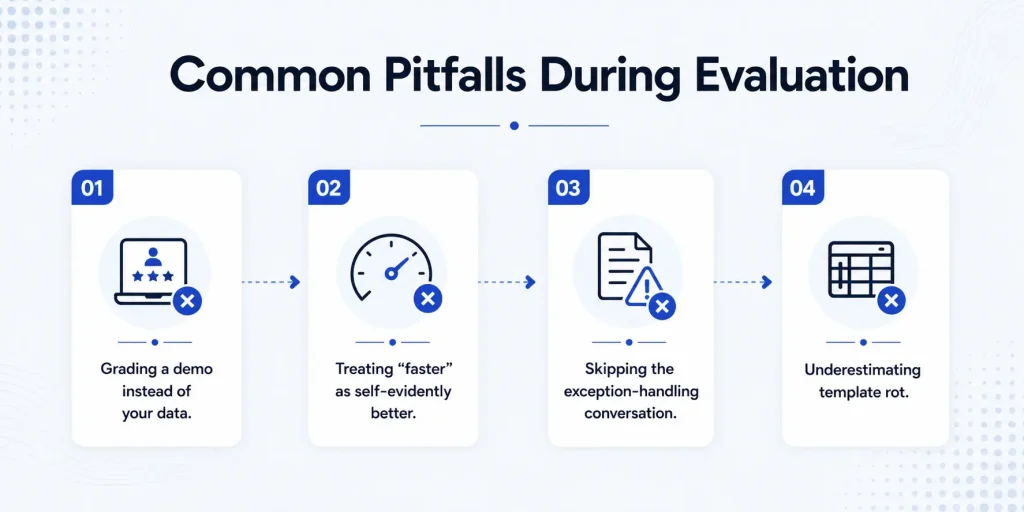

Common Pitfalls During Evaluation

- Grading a demo instead of your data. Vendor sample data is clean by design. Test reconciliation against your messiest account, not their best one.

- Treating “faster” as self-evidently better. Ask what got faster and why. If nobody in the room can explain why, that’s the question to keep asking.

- Skipping the exception-handling conversation. Most demos show the happy path. Ask explicitly: “walk me through what happens when something doesn’t match.”

- Underestimating template rot. Ask whether the platform can flag recurring entries that have not been reviewed since a defined trigger, such as an acquisition, a new revenue stream, or a chart-of-accounts change.

Where to Go From Here

The point of evaluating month-end close automation isn’t to find the platform that promises the shortest close. It’s to find the one that makes it harder for close debt to accumulate quietly – one that treats every exception, every stale template, and every uninvestigated variance as something to surface rather than as something to smooth over.

If you’re building a shortlist, run each vendor through the close-debt questions in the table above using your actual chart of accounts, not their demo environment. The vendors that welcome that conversation are worth a longer look. The ones that redirect back to the day count are telling you something too.