Key Takeaways

- Regulatory reporting automation is less about speed and more about risk reduction, especially in cross-geography environments where inconsistencies compound quickly.

- Most reporting risks come from missing context and fragmented evidence, not from incorrect calculations.

- Traditional automation improves efficiency but often fails to ensure traceability and explainability, shifting risk to audit stages.

- Embedding validation and evidence directly into workflows is critical to achieving consistent, audit-ready reporting.

- AI can enhance regulatory reporting, but without governance and structured processes, it can introduce new risks instead of reducing them.

Manufacturing finance leaders usually don’t worry about report generation. They worry about whether those reports will stand up to scrutiny.

That distinction matters more than most automation conversations acknowledge.

Across geographies, regulatory reporting is not just a data aggregation exercise. It’s a test of consistency, traceability, and interpretation—often across systems that were never designed to agree with each other. When organizations discuss regulatory reporting automation, the conversation tends to orbit efficiency: faster submissions, fewer manual steps, and lower operational cost.

Useful, yes. But not the real prize. The real prize is reduced risk—specifically, the risk of being wrong, inconsistent, or unable to explain why a number exists in the first place.

And that’s where things become complicated.

The Illusion of Standardization in Global Reporting

On paper, global finance functions look standardized. IFRS or GAAP frameworks, centralized ERP systems, shared service centers—it all suggests a level of uniformity.

In practice, it’s anything but.

A manufacturing group operating across the EU, India, and the US might be dealing with:

- Local statutory adjustments layered on top of global reporting standards

- Country-specific disclosures that don’t map cleanly to group templates

- Different interpretations of similar accounting treatments

- Regulatory timelines that don’t align (and sometimes conflict)

Even something as straightforward as revenue recognition can diverge subtly between jurisdictions. The discrepancy may not be significant enough to cause immediate alarms, but it can lead to reconciliation issues in the future.

So when companies attempt regulatory reporting automation, they often start from a flawed assumption: that the underlying data is already harmonized.

It isn’t. And automating inconsistency tends to amplify it.

Where Risk Creeps In

Risk in regulatory reporting doesn’t usually come from large, obvious errors. Those get caught. It’s the smaller, compounding inconsistencies that slip through.

A few patterns show up repeatedly:

1. Data Transformation Without Context

Numbers move between systems—ERP to consolidation tool, consolidation to reporting platform—but the logic behind transformations isn’t always preserved.

Someone, somewhere, applied a rule. Maybe it made sense at the time. Six months later, nobody remembers why.

During audits, this becomes a problem:

- “Why was this adjustment applied only to Entity X?”

- “What triggered this classification change?”

If the answer lives in a spreadsheet comment or a departed employee’s memory, risk has already materialized.

2. Local Overrides That Don’t Scale

Regional teams often apply manual adjustments to meet local compliance needs. It’s practical in the moment.

But across 10–15 entities, those overrides start behaving unpredictably:

- Same transaction treated differently in two jurisdictions

- Adjustments applied twice (once locally, once at group level)

- Reversals that never quite reverse fully

Automation doesn’t eliminate these issues—it can actually harden them if not designed carefully.

3. Evidence Gaps

This is the one that tends to get underestimated.

Regulatory bodies don’t just want numbers. They want evidence:

- Supporting documents

- Approval trails

- Justification for judgments

In many organizations, that evidence is scattered:

- Email threads for approvals

- Shared drives for documents

- ERP logs for transactions

When a regulator asks for clarification, finance teams don’t retrieve evidence—they reconstruct it. That reconstruction is slow, error-prone, and frankly, avoidable.

Also read: Raw Material Price Monitoring with AI Agents

Why Traditional Automation Only Solves Half the Problem

Most regulatory reporting automation initiatives focus on process efficiency:

- Automating data extraction

- Standardizing report formats

- Scheduling submissions

- Reducing manual consolidation work

All of which are necessary. But they miss a critical layer: explainability.

A report generated in minutes is still risky if:

- The underlying logic isn’t transparent

- Adjustments aren’t traceable

- Supporting evidence isn’t linked

There’s a subtle but important shift here. Automation that prioritizes speed without traceability doesn’t reduce risk—it redistributes it. This shift often occurs from operations to the audit and compliance teams. And those teams notice.

A More Practical View of Regulatory Reporting Automation

If reduced risk is the goal (and it should be), then automation needs to address three dimensions simultaneously:

1. Data Consistency Across Entities

Not just standardized formats, but aligned definitions.

For example:

- What qualifies as “capital expenditure” in one region should mean the same elsewhere

- Currency conversions should follow consistent methodologies

- Classification rules should not depend on who is processing the data

This statement sounds obvious. It rarely is.

2. Embedded Validation, Not Post-Processing Checks

Many organizations still rely on validation as a downstream activity:

- Generate report

- Review exceptions

- Fix discrepancies

A more robust approach embeds validation earlier:

- At data entry

- During transformation

- Before consolidation

This reduces the volume of exceptions later and, more importantly, ensures issues are caught closer to their source.

3. Evidence as Part of the Workflow

This is where most implementations fall short. Evidence is treated as an attachment, not an integral component.

A more resilient model:

- Captures approvals within systems (not via email)

- Links supporting documents directly to transactions

- Maintains version history of changes

- Generates audit trails automatically

Cross-Geography Complexity Isn’t Just Technical

It’s tempting to frame the issue as a systems problem. Occasionally it is. But often, it’s organizational.

Different regions operate with different assumptions:

- Some prioritize speed over documentation

- Others emphasize compliance rigor

- Some rely heavily on informal communication

Trying to impose a single global model without accounting for these differences usually backfires.

A better approach acknowledges the variability:

- Define minimum evidence and validation standards

- Allow controlled flexibility for local requirements

- Monitor deviations rather than eliminating them entirely

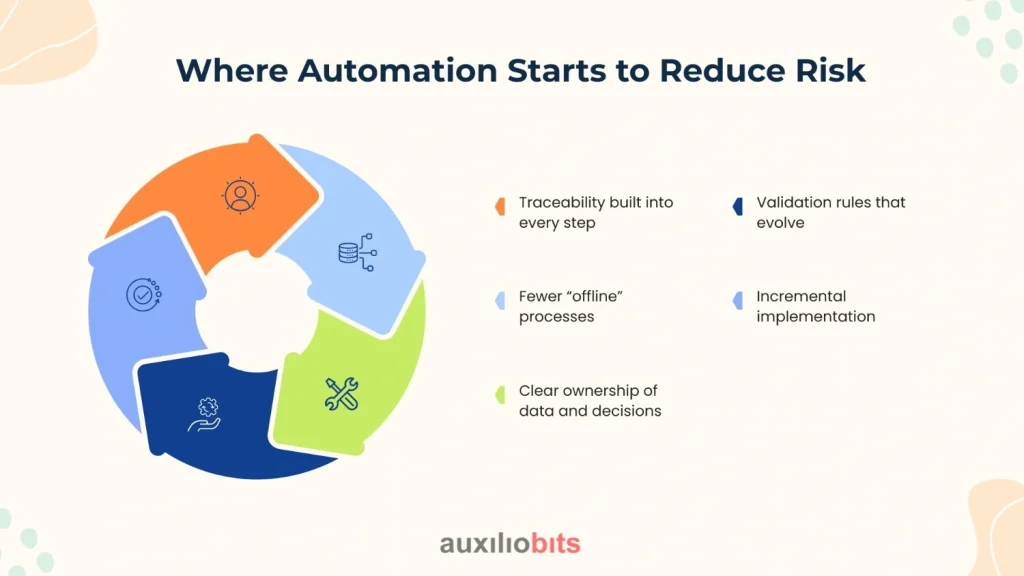

Where Automation Starts to Reduce Risk

When done thoughtfully, regulatory reporting automation can materially reduce risk. Not eliminate it—but make it manageable.

A few patterns that tend to deliver results:

- Traceability built into every step: Transactions, adjustments, and approvals are linked. Not inferred later.

- Validation rules that evolve: Static rules break in dynamic environments. Systems need to adapt to new regulatory requirements without constant rework.

- Fewer “offline” processes: The more activity happens outside core systems, the harder it is to maintain consistency.

- Clear ownership of data and decisions: Automation doesn’t remove accountability. If anything, it makes gaps more visible.

- Incremental implementation: Trying to automate everything at once often leads to fragile systems. Starting with high-risk areas tends to be more effective.

The Role of AI And Where It Helps

There’s a lot of noise around AI in finance. Some of it is justified. Some of it… optimistic.

In the context of regulatory reporting, AI is useful in specific areas:

- Interpreting unstructured data (contracts, regulatory updates)

- Identifying anomalies that rule-based systems might miss

- Assisting in classification and mapping tasks

But AI doesn’t replace the need for:

- Clear policies

- Defined workflows

- Strong governance

Without those, AI can introduce new risks—particularly around explainability. And regulators are not known for their tolerance of “black box” decisions.

A Shift in How Finance Teams Should Think About Risk

Traditionally, risk in reporting has been viewed as something to be managed at the end:

- Final reviews

- Audit checks

- Compliance validations

But in multi-entity, cross-geography environments, that model struggles.

Risk needs to be managed continuously:

- At the point of data creation

- During every transformation

- Across every handoff between systems and teams

It’s less about catching errors and more about preventing ambiguity.

Where Many Initiatives Still Go Off Track

Even with the right intent, a few things tend to derail automation efforts:

- Over-standardization: Trying to force identical processes across all regions can create resistance—and workarounds.

- Too much reliance on ERP capabilities: Most ERP systems weren’t designed for cross-geography reporting complexity at this level.

- Ignoring behavioral change: Moving from email-based approvals to system-driven workflows isn’t just a technical shift.

- Treating evidence as optional: It never is. It just becomes urgent later.

Bringing It Back to Reduced Risk

If there’s one thread running through all of this, it’s that regulatory reporting automation only delivers real value when it reduces uncertainty.

Not just faster reporting. Not just cleaner templates.

But:

- Clear lineage of data

- Consistent application of rules

- Immediate access to supporting evidence

- Confidence that numbers can be explained—not just presented

That’s what reduces risk. Everything else is secondary.

A Final Thought

Manufacturing organizations aren’t short on systems. They’re not even short on automation. What they often lack is alignment—between data, processes, and evidence. Until that alignment exists, regulatory reporting will continue to feel heavier than it should. Automation will help, but only up to a point.

Beyond that, it’s not about doing things faster. It’s about making sure they make sense.