Key Takeaways

- ESG reporting failure in manufacturing is rarely about intent—it’s driven by fragmented, disconnected data ecosystems.

- Manual processes don’t just slow things down; they quietly introduce inconsistencies that compound over time.

- Spreadsheets and email-based workflows create more risk than control at enterprise scale.

- Supplier and external ESG data remain one of the weakest—and least governed—links in reporting.

- Fixing ESG reporting isn’t about better reports; it’s about rethinking how data is structured, integrated, and governed across the organization.

There’s a quiet tension in most manufacturing boardrooms right now. On one side, ESG reporting has moved from “nice-to-have” to regulatory expectation. On the other, the actual machinery of reporting—the data, the workflows, the ownership—still looks like it did ten years ago.

Spreadsheets. Emails. Shared drives. A few dashboards stitched together with noble intentions.

And then leadership wonders why ESG reporting failure keeps showing up in audits, investor conversations, and sustainability disclosures.

The truth? It’s not just about effort or intent. Manual approaches fail because the underlying data landscape in manufacturing is fundamentally fragmented—and ESG reporting simply exposes that weakness.

The Illusion of Control in Manual ESG Reporting

Most operations or sustainability teams will provide a confident answer when you enquire about the management of ESG data. There are templates. Defined owners. Monthly or quarterly cycles.

On paper, it feels structured. In reality, it’s something closer to controlled chaos.

A typical reporting cycle might look like this:

- Energy consumption pulled from plant-level systems

- Emissions data calculated separately using conversion factors

- Water usage tracked in local logs (sometimes digital, sometimes not)

- Supplier ESG metrics collected via email surveys

- Waste data maintained by EHS teams in isolated tools

None of these practices is inherently wrong. In fact, many organizations have matured these processes over time. But the problem isn’t within each dataset—it’s between them. Human effort assumes that these disconnected pieces can be reliably stitched together in manual ESG reporting. That assumption doesn’t hold at scale.

Also read: Revenue Leakage in Manufacturing—and How Automation Fixes It

Data Fragmentation: The Root Cause Nobody Owns

Let’s be precise here. Data fragmentation in manufacturing isn’t new. It’s structural. Different plants operate semi-independently. Systems vary by geography, acquisition history, or operational maturity. Even within a single facility, production, maintenance, and compliance teams often use different tools.

Now layer ESG on top of that. You’re no longer just tracking operational metrics—you’re trying to correlate them:

- Energy consumption with production output

- Emissions with specific processes

- Supplier practices with procurement decisions

- Waste streams with lifecycle impacts

That requires a level of data cohesion that most manufacturing environments simply don’t have. And so, people compensate.

They manually reconcile. They interpret. They make assumptions where data doesn’t align.

It works—until it doesn’t.

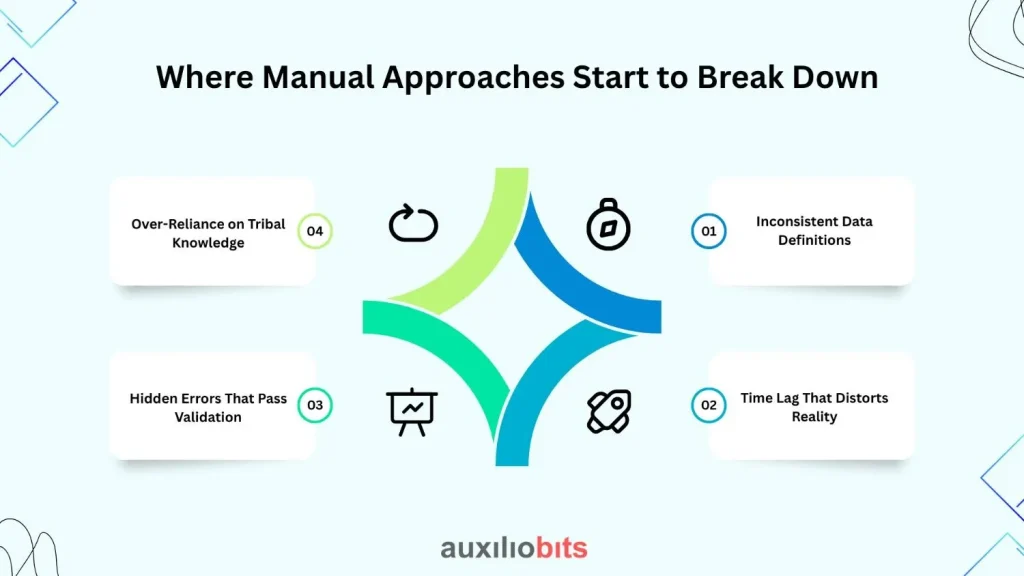

Where Manual Approaches Start to Break Down

It’s tempting to think ESG reporting failure is about scale. That things work fine until the organization gets “too big”.

That’s partially true, but it misses the nuance. Manual approaches don’t just fail at scale—they fail under complexity.

Here’s where cracks start to show:

1. Inconsistent Data Definitions

What qualifies as “energy consumption” in one plant may not match another.

- Does it include backup generators?

- Are renewable sources tracked separately?

- Are estimates used when meters fail?

Without standardized definitions, aggregated reports become misleading. The reports may not be blatantly incorrect, but they exhibit subtle inconsistencies. And those inconsistencies compound over time.

2. Time Lag That Distorts Reality

Manual reporting introduces delays. Data is collected, validated, adjusted, and finally reported—often weeks after the fact. By the time leadership sees ESG metrics, they’re looking at a historical artifact, not an operational signal.

That lag has real consequences:

- Missed opportunities to reduce emissions in real time

- Delayed response to compliance risks

- Inability to link sustainability performance with operational decisions

It’s like driving using last month’s GPS data.

3. Hidden Errors That Pass Validation

Here’s something practitioners don’t always admit openly: most ESG reports contain errors. Not catastrophic ones. Small discrepancies. A unit conversion mistake. A duplicated entry. A missed update in a shared file.

Manual processes rely heavily on human validation, which is inherently inconsistent. Even with multiple review layers, errors slip through—especially when data is fragmented across sources.

And because ESG data is often aggregated, these errors are challenging to trace back.

4. Over-Reliance on Tribal Knowledge

In many organizations, ESG reporting depends on a few key individuals who “know how things work”.

They understand:

- Which data sources are reliable

- How to interpret anomalies

- What adjustments are typically made

That knowledge isn’t documented—it’s accumulated. So what happens when those individuals leave, change roles, or simply become overloaded?

The process doesn’t just slow down. It degrades.

Why Spreadsheets Become the Bottleneck

Spreadsheets deserve some credit—they’ve carried enterprise reporting for decades. But ESG reporting pushes them beyond their limits.

The issue isn’t just volume. It’s structure.

Spreadsheets:

- Lack enforceable data standards

- Struggle with real-time integration

- Depend on manual version control

- Offer limited traceability for audit purposes

At some point, they stop being tools and start becoming risks. Yet many organizations hesitate to move away from them. Why? Because spreadsheets provide flexibility. And in a fragmented data environment, flexibility feels necessary. It’s a trade-off—control versus adaptability. Most teams choose adaptability, even if it introduces long-term risk.

The Supplier Data Problem

Internal data fragmentation is one challenge. Supplier data adds another layer entirely. Manufacturers increasingly need ESG metrics from suppliers:

- Emissions data

- Labor practices

- Resource usage

- Compliance certifications

This data is usually not standardized. It arrives in different formats, levels of detail, and degrees of reliability.

Manual approaches try to manage the information through:

- Email questionnaires

- Self-reported spreadsheets

- Periodic audits

The result? A patchwork of data that’s difficult to validate and even harder to integrate.

And yet, this data often feeds directly into ESG disclosures. There’s a certain irony here—companies invest heavily in internal accuracy while relying on loosely verified external inputs.

When Compliance Pressure Meets Operational Reality

Regulatory expectations around ESG are tightening. Frameworks are becoming more detailed. Audits are becoming more rigorous.

Manual processes struggle under this pressure. Not because teams aren’t capable—but because the system they’re working within isn’t designed for it.

You start to see patterns:

- Last-minute data corrections before disclosures

- Increased audit findings related to data inconsistencies

- Growing disconnect between reported metrics and operational reality

At some point, reporting becomes an exercise in reconciliation rather than reflection. And that’s where credibility starts to erode.

What Works?

There’s a tendency to frame this as a technology problem. Just implement a platform, integrate systems, and everything improves.

It’s not that simple. Technology helps—but only if it addresses the underlying issue: fragmented data.

Some approaches that tend to work:

- Standardizing data definitions first, before automating collection

- Building integration layers that pull data from existing systems rather than replacing them

- Establishing clear ownership at the data level, not just at the reporting level

- Automating validation rules to catch inconsistencies early

And just as importantly, recognizing what doesn’t work:

- Lifting manual processes into digital tools without redesigning them

- Over-engineering solutions that require perfect data (which rarely exists)

- Treating ESG reporting as a standalone function rather than an extension of operations

A Subtle but Critical Shift: From Reporting to Data Architecture

Here’s where perspective matters. Most organizations approach ESG as a reporting challenge.

But the more experienced ones start to see it differently—it’s a data architecture problem. Reporting is just the output.

The real work happens upstream:

- How data is generated

- How it’s structured

- How it flows across systems

- How inconsistencies are handled

Once you fix that, reporting becomes significantly easier—and more reliable. Ignore it, and no amount of manual effort will compensate.

The Cost of Doing Nothing

It’s easy to delay change. Manual processes, after all, do produce reports.

But there’s a cost to maintaining the status quo:

- Increasing effort for each reporting cycle

- Growing risk of non-compliance

- Reduced confidence from stakeholders

- Missed opportunities to link ESG performance with operational improvements

And perhaps most importantly—decision-making based on imperfect data. That last one is often underestimated. ESG metrics aren’t just for disclosure; they’re increasingly used to guide strategy.

If the data is fragmented, the strategy built on it won’t hold.

A Final Thought

There’s a pattern that has been noticed repeatedly. Organizations don’t abandon manual ESG reporting because they want to innovate. They do it because the cracks become impossible to ignore.

An audit finding. A failed disclosure. A leadership question that can’t be answered confidently. Something breaks. Until then, manual processes persist—not because they’re effective, but because they’re familiar.

The irony is that ESG reporting manufacturing challenges aren’t really about ESG at all. They discuss how data moves—or doesn’t—within the enterprise.

Addressing that issue will help many other aspects to align more effectively. Failure in ESG reporting is only the beginning if you ignore it.