Key Takeaways

- Agents move personalization from static segmentation to continuous context awareness, enabling banks to respond to customer intent, timing, and friction in real time without redesigning journeys or campaigns.

- True hyperpersonalization is often invisible, showing up as reduced friction, fewer interruptions, and smarter restraint rather than more offers, messages, or features competing for customer attention.

- Timing consistently outperforms targeting, as agents monitor micro-behaviors and act only when an intervention adds situational value instead of blindly following eligibility rules or campaign calendars.

- Agentic systems replace fixed journeys with adaptive paths, allowing digital banking experiences to bend around customer behavior, hesitation, and comprehension rather than forcing linear, predesigned flows.

- The real impact of agents is cultural, not cosmetic, shifting banks from product-push thinking toward decision-making models optimized for trust, long-term engagement, and value creation under uncertainty.

Digital banking teams talk about personalization constantly. More teams fail to experience it in production, at scale, while maintaining compliance, latency budgets, and customer trust.

Most “personalization” in banking today is still about wearing better clothes. Segment-based offers. The customer journeys remain static and unchanging. Decision trees were designed months ago and are rarely revisited because touching them requires legal sign-off, QA cycles, and a small miracle. It works—until it doesn’t. And customers notice.

Agents change this dynamic in ways that are subtle at first and disruptive once you see them clearly.

This isn’t about chatbots replacing call centers. It’s about agentic systems quietly reshaping how banks understand intent, context, and timing—often across dozens of interactions that never surface as a single “experience” slide in a deck.

Why HyperPersonalization Has Been So Hard in Banking

Banks are information-rich and insight-poor at the same time. They know balances, transactions, credit history, channel usage, device fingerprints, and behavioral patterns stretching back years. Yet translating that into relevant, moment-specific engagement has always been constrained by a few stubborn realities.

- Regulatory oversight discourages improvisation

- Core systems weren’t designed for real-time decisioning

- Personalization logic is fragmented across teams and tools

- “Next best action” engines tend to ossify quickly.

A credit card upsell might be technically personalized (“customer has income > X”), but it rarely feels personal. It ignores mood, timing, friction, and intent. It doesn’t ask: Why is the customer here right now? Or even better: Should we intervene at all?

This is where agent-based architectures quietly outperform traditional orchestration models.

What Banking Agents Actually Are

When people hear “agents,” they often picture a conversational UI. That’s a surface, not the system.

In digital banking, agents are autonomous or semi-autonomous software entities that:

- Observe signals across channels (app behavior, transaction events, prior interactions).

- Reasoning over context using models, rules, and memory

- Decide whether to act, defer, escalate, or stay silent

- Execute actions across systems—within predefined guardrails

Sometimes they speak. Often they don’t.

A fraud-monitoring agent that decides not to interrupt a legitimate transaction because it understands customer travel patterns is still personalizing the experience—by reducing friction rather than adding features.

That’s an important nuance. Hyperpersonalization isn’t always visible.

Also read: Automating KYC and AML Compliance in Banking with UiPath

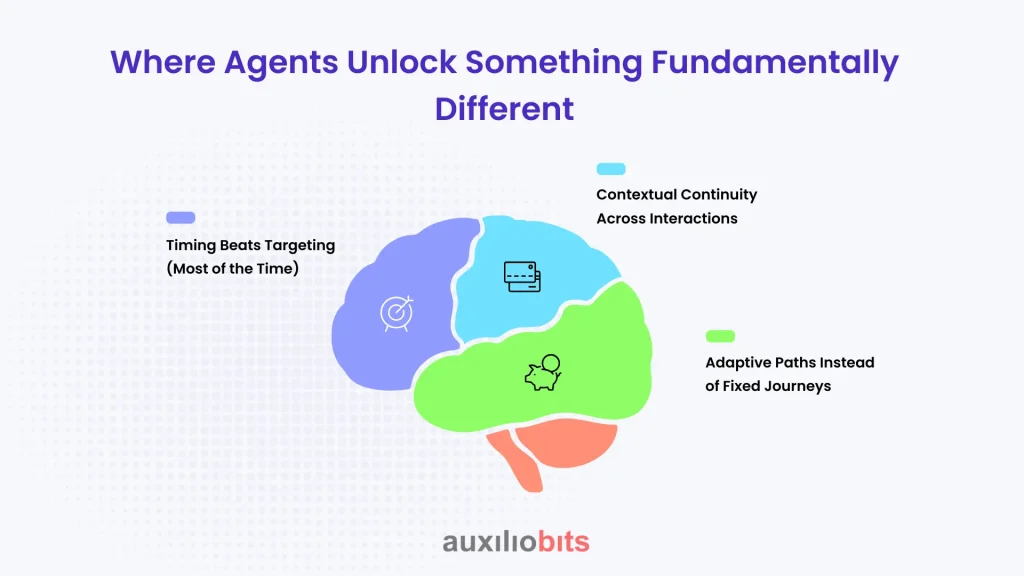

Where Agents Unlock Something Fundamentally Different

Traditional personalization engines ask: What offer fits this profile? Agents ask: What outcome are we optimizing for right now, given everything we know?

That difference shows up in a few concrete ways.

1. Contextual Continuity Across Interactions

Most banking journeys are broken across sessions. A customer researches a loan today, checks their balance tomorrow, and calls support next week. These are treated as separate events.

Agents maintain continuity.

A lending agent can remember that a customer abandoned a mortgage calculator after seeing estimated closing costs—then quietly adjust future messaging to focus on affordability tools instead of promotional rates. No campaign needed. No CRM workflow update.

Some banks already do this well in pockets. DBS, for example, has spoken publicly about using behavioral context—not just demographics—to shape engagement flows. What’s changing now is that agents can reason over this context continuously rather than triggering isolated rules.

2. Timing Beats Targeting (Most of the Time)

Marketing teams obsess over targeting accuracy. Agents obsess over timing.

An overdraft-protection offer sent at the wrong moment feels predatory. The same suggestion, delivered when a customer is actively managing cash flow, feels helpful. Agents monitor micro-signals:

- Rapid balance checks late at night

- Repeated navigation between bills and savings

- Small, frequent transfers before payroll hits

These patterns aren’t new. What’s new is the ability for an agent to act—or deliberately not act—without waiting for a batch job or campaign window.

Sometimes the best personalization is restraint.

3. Adaptive Paths Instead of Fixed Journeys

Journey maps look great in workshops. Real customers don’t follow them. Agents don’t assume linearity. They adjust paths based on resistance, confusion, or hesitation. If a customer repeatedly ignores educational nudges about investing but engages deeply with tax-related content, the agent recalibrates. There is no need for reconfiguration.

This matters in complex products—wealth management, SME lending, insurance riders—where comprehension varies widely. Agents allow the experience to bend instead of break.

A Subtle Shift in How Banks Think About Customers

Agent-driven hyperpersonalization nudges banks away from asking, “What can we sell?” toward a more situational question: “What does this customer need right now—if anything?”

That distinction matters more than it first appears. Product calendars, campaign quotas, and eligibility logic have shaped digital banking experiences for years. Agents introduce a different center of gravity. Decisions are no longer driven solely by what the bank wants to promote but by whether an intervention adds value in the moment. The shift sounds philosophical, yet its consequences are practical, observable, and measurable in everyday customer behavior.

What This Shift Looks Like in Practice

| Traditional Digital Banking Approach | Agent-Driven Hyperpersonalization | Resulting Customer Perception |

| Prompts triggered by product eligibility or campaign timing | Actions triggered by real-time behavioral and contextual signals | Fewer messages that feel irrelevant or poorly timed |

| Engagement optimized for visibility and frequency | Engagement optimized for situational usefulness | Higher interaction quality without aggressive nudging |

| Static journeys designed upfront | Adaptive flows that adjust based on resistance or intent | Experiences that feel responsive rather than scripted |

| Consistency enforced through rigid rules | Consistency achieved through contextual decisioning | Predictable behavior without repetitive prompts |

| Novel features used to capture attention | Restraint used to preserve trust | An app that intervenes only when it adds value |

| Sales success measured by conversion volume | Success measured by long-term engagement and reduced friction | Less fatigue, more willingness to engage |

| Customers conditioned to ignore in-app messages | Customers learn that prompts are usually relevant | Trust built through relevance, not persuasion |

We’re likely to see agents move upstream—from engagement into product design itself. Features that reconfigure based on usage patterns. Pricing models that adapt within predefined fairness bands. Support experiences that feel less like queues and more like conversations that pick up where you left off.

Not every bank will get this right. Some will overreach. Others will move too cautiously and cede ground to more adaptive competitors.

The quiet winners will be the ones who treat agents not as a feature, but as an operating model for decision-making under uncertainty.

Hyperpersonalization isn’t about dazzling customers. It’s about respecting their context enough to know when to act—and when not to.

That’s harder than it sounds. And that’s why agents matter.